Opening a savings account is one of the most straightforward things you can do for your financial health. The harder part is knowing how to use it. Should the money be for emergencies? A specific goal? Both at once? The answer matters more than most people realize, and getting clear on it changes how consistently you save.

Most people fall into one of two camps: they save with no real target in mind, or they are holding out for a single big goal and ignoring everything else. A better approach is to do both at once, building a cushion that catches you when life goes sideways while also working toward the things you want.

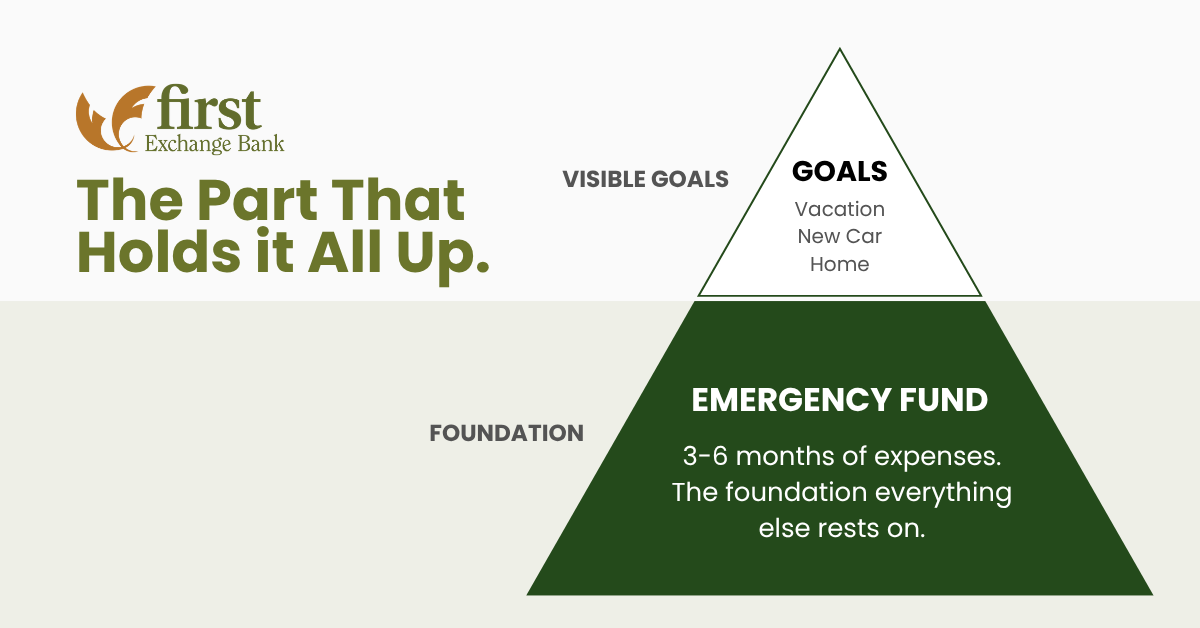

What a Savings Account Is Actually For

A savings account sits in the middle ground. It is more accessible than CDs, which restrict when you can access your money, but more separated from daily life than a checking account, where every dollar is one swipe away. That distance is the point. Money you cannot accidentally spend has a better chance of still being there when you need it.

People use savings accounts to:

- Build an emergency fund

- Save for purchases, vacations, or education

- Make a down payment for a mortgage

- Develop healthy financial habits

You could try to manage all of this from a single checking account. Some people do. Most find that without a physical separation between spending money and saving money, the saving slowly disappears.

Why an Emergency Fund Comes First

A car repair. A medical bill. A week without pay. These things happen to almost everyone, and they tend to arrive at the worst possible time. Without a savings cushion, the only options are often credit cards or loans, and borrowing to cover an emergency means paying interest on top of an already stressful situation. An emergency fund breaks that cycle before it starts.

How much is enough?

The standard guidance is three to six months of living expenses, enough to keep you stable if your income stops for a while. If that number feels out of reach, start with $1,000. It will not cover everything, but it will cover most of the unpleasant surprises that come along in a normal year. The goal is to start, not to start big.

![]()

Saving for Goals: Turning Something You Want into Something You Have

Once you have a foundation in place, a savings account can become a tool for building the future you want, not just protecting against the one you fear.

People save for homes, cars, vacations, education, holiday spending, and anything else they would rather not put on a credit card. The goal itself matters less than the act of naming it. Vague intentions to save “for the future” are easy to ignore. A labelled account with a target balance and a deadline is much harder to abandon.

Watching a balance climb toward a number you chose creates a different kind of motivation than watching a general savings account slowly grow. Progress is visible, and visible progress tends to continue.

You Do Not Have to Choose Between Safety and Goals

The most common mistake is treating these as competing priorities. People hold off on goal-based saving until the emergency fund is complete, or they skip the emergency fund entirely because the goal feels more exciting. Both approaches leave you exposed.

A better approach is to run both simultaneously, even if the splits are uneven at first. When money is tight, direct more to the emergency fund. As that stabilizes, shift more toward goals. The strategy should flex with your circumstances.

Practical Ways to Make It Work

These approaches work regardless of income level or how far behind you feel.

Automate Your Savings

Automatic transfers remove the decision entirely. Set up a transfer on payday and the money moves before you think about spending it. Even a small recurring transfer builds real savings over time.

Start Small and Increase Gradually

There is no minimum that matters. Twenty-five dollars per paycheck is a real savings habit. Starting there and increasing gradually beats waiting until you can save a larger amount.

Save Windfalls and Extra Income

A tax refund, a bonus, or any unexpected income is an opportunity to jump ahead. Putting even half of a windfall into savings can accelerate your timeline significantly without changing how you live day to day.

Review Your Budget Regularly

A monthly review of spending often reveals money going places you have not noticed. Small adjustments add up without requiring a significant change in how you live.

Mistakes That Quietly Slow Your Progress

Keeping Savings Too Accessible

Savings that live in your checking account tend to get spent. A dedicated savings account, separate from your daily spending, creates the distance needed to let money accumulate.

Not Having Specific Goals

Saving for “someday” or “the future” rarely works as well as saving for something specific. A named goal with a number attached gives you something to track and a reason to keep going.

Waiting for the “Perfect Time” to Start

Financial security rarely arrives on its own. It is usually built gradually, starting with an amount that feels almost too small. Waiting for the right moment is the same as not starting.

Why a Community Bank Makes a Difference

At a large national bank, a savings question usually goes to a call center. At First Exchange, it goes to someone who lives and works in North-Central West Virginia and understands what financial life here actually looks like.

That matters when you are trying to build something real. We offer:

- Bankers who know this community personally, not just professionally

- Branch locations in White Hall, Mannington, Fairmont, Fairview, Hundred, and Morgantown

- Long-term relationships built on knowing customers by name

- Guidance tailored to your situation, not a script

When you have a question about which account fits your goals, or whether your savings plan makes sense, you can walk in and talk to someone who can actually help you think it through.

Ready to Open a Savings Account? Here Is Where to Start.

Whether you are just getting started or looking to organize savings you already have, we can help you find the right account and set up a plan that works.

We offer several savings options built for different situations, including Statement Savings, Money Market accounts, Certificates of Deposit, a Christmas Club Account, Youth Savings Accounts, and IRAs. Every account comes with:

- Personalized support from a local banker who knows your name

- Easy-to-use online banking tools

- Branch locations throughout North-Central West Virginia

- A variety of savings and checking accounts

{kind=link}

Stop by any of our locations locations or contact us to talk through your options. We will help you figure out the right accounts for where you are now, and where you want to go.

Start Where You Are

The best savings plan is the one you can consistently follow.

Start with an emergency cushion, name a goal, automate a transfer, and review it every month. That is the whole strategy. The amount you start with matters far less than the habit of starting.

First Exchange Bank is here whether you are opening your first savings account or reorganizing one you have had for years. Contact us today to open a savings account or talk through which option fits your situation.